Tom Konrad, Ph.D., CFA

I don’t spend much time reading investment company ESG reports, but a friend asked me to take a look at a copy of the TIAA’s 2021 Climate Report. I was deeply unimpressed. Here are a few things in the report that triggered my greenwashing radar:

- TIAA wants to work with companies to improve their behavior. They call this company engagement. “[W]e do not expect [asset sales] to account for the majority of our emissions reduction — we are primarily focused on company engagements” page 9.

- Much of TIAA’s emphasis is on reducing emissions from their own operations, rather than the companies they invest in. For an investment company, the greenhouse impact of its offices and computers are tiny compared to the impacts of the companies that it invests in.

- While TIAA has set greenhouse gas reduction targets for the assets it owns directly, it also manages over four times as much money for other investors. The report completely ignores the greenhouse gas impacts of these investments.

- Where TIAA does have targets, they are long term, for 2040 and 2050. We need to act now, not in a decade or two.

Given the urgency of the climate crisis– “Code red for humanity” as the UN Secretary General puts it– incremental change falls so short of the need that it’s difficult to consider it green.

Why Company Engagement Doesn’t Cut It

At best, working with companies to improve their behavior will produce incremental change. Do we really see an oil company completely ceasing new development of fossil fuels, and phasing down its current operations over the next 20 years because of shareholder engagement? The idea seems laughable, but that is exactly what an oil company would have to do if it plans to be part of the solution, not just a smaller part of the problem. Even the most ambitious oil majors, like BP (NYSE:BP) are just hoping to reduce the emissions from their own operations to zero by 2050. If they are still producing oil after 2050, they are part of the problem.

Engaging with companies to try to get them to reduce carbon emissions is better than nothing, but stronger measures are needed. The potential gains from shareholder engagement are fine if a company only needs to make small changes to reduce its greenhouse gas emissions, but stronger measures are needed when a company’s core business causes climate change. If an investment management company wants to help solve the problem of climate change, the only real solution is to sell companies (like coal, oil, and gas producers,) whose core business causes climate change.

Too Little

The difference between powering your computer with renewable electricity and powering your computer with electricity generated from coal is negligible if what you do with that computer is buy shares in Exxon Mobil (NASD: XOM).

Like an oil company that has a target to reduce the emissions from its own operations to zero, while ignoring the emissions when its customers burn the fuels it produces, an investment management company that reduces its own emissions while ignoring the emissions of the companies it invests in is missing the point. TIAA is doing just that.

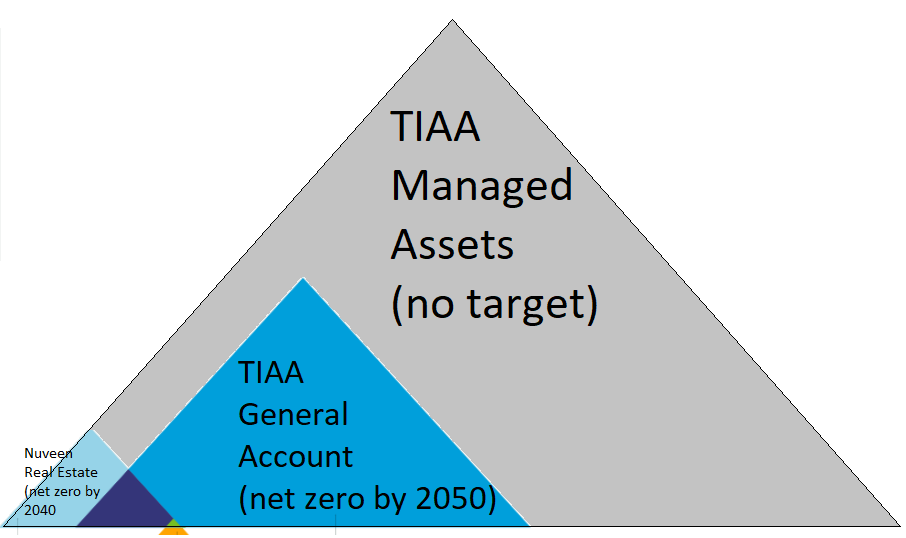

Apparently without intended irony, TIAA included the following diagram of its emissions targets in its report (slide 17):

The tiny orange/green triangle represents the carbon emissions from TIAA’s own operations (i.e the power that heats and cools its offices and powers its computers.) The larger blue triangles represent the financed emissions from the assets which TIAA owns directly. The (even larger) financed emissions from the companies owned by TIAA mutual funds and other investment products are not even shown. (TIAA has $1.3 trillion under management. The general account and real estate assets shown in the diagram are only about a quarter of that… and still they make the emissions from TIAA’s own operations look insignificant.)

In short, TIAA’s climate targets only encompass about a quarter of the carbon emissions from the investments it manages… the ones where it has the most control. A more accurate picture of the relevant sizes of TIAA’s targets (and lack thereof) would be shown in the expanded diagram below:

(Diagram by author. Large gray triangle drawn as approximately 4x the area of the TIAA general account, to reflect the relative sizes of TIAA’s assets under management.)

(Diagram by author. Large gray triangle drawn as approximately 4x the area of the TIAA general account, to reflect the relative sizes of TIAA’s assets under management.)

Too Late

Even if TIAA’s targets covered all of its assets under management, including only 2040 and 2050 targets without significant shorter term goals means that these targets fall far short of what we need to accomplish to avert the worst effects of climate change.

According to the International Panel on Climate Change, the entire world (and hence all assets which TIAA invests in, including those it manages for others) needs to produce net zero carbon emissions by 2050. To get there, we can’t leave most of the work until the last few years. We need to make significant progress by 2030. For TIAA, this might mean moving up its 2040 net zero targets (Nuveen Real Estate and its own operations) to 2030, its 2050 target for the general account to 2040, and setting additional targets for the funds it manages for others to be one third of the way to net zero by 2030, two thirds by 2040, and at net zero by 2050.

That’s what it would take for TIAA to stop being part of the problem.

To be part of the solution, green money management leaders go much further. A net zero portfolio can be built today. We also actively invest in the companies that will help the world get to net zero, and avoid the major greenhouse gas emitters entirely. Not everyone can lead, so I’ll be happy if TIAA just stops being part of the problem. The sooner the better.

DISCLOSURE: No positions in any companies mentioned.

{kind=link}